Finance Project (designed by Melanie Lorek, City Tech QR Fellow)

Click here to download the FinanceProject (PDF)

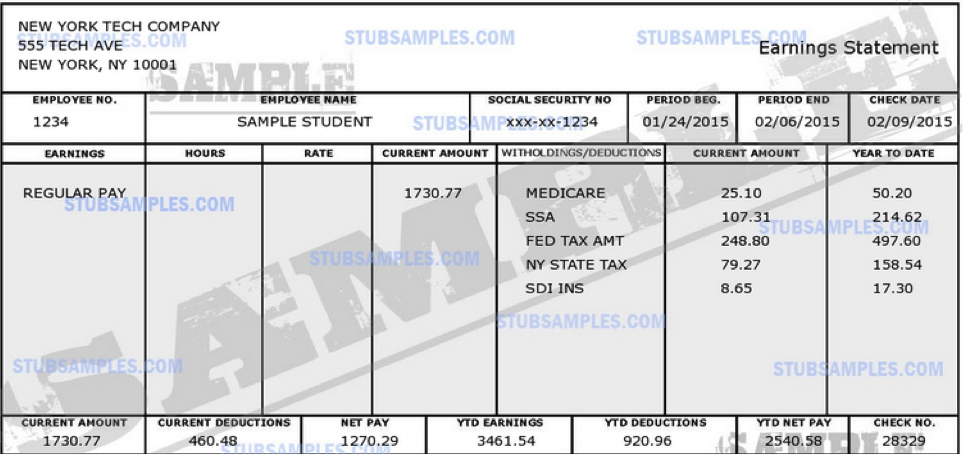

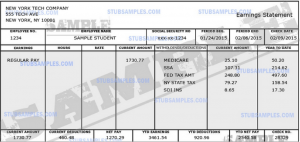

After graduating from NYCCT you landed a job earning 45k/ year. Congrats! Now it’s time to think about your long term life goals. Do you want to buy a car, a house, save for retirement, and attend grad school? Based on the information below and your bi-weekly income displayed in the pay stub below, compute the monthly costs for each scenario, and how long it would take to pay off each item. Remember that you’ll also have to pay off your student loan, and will need to cover your everyday living expenses.

This assignments consists of several steps:

- Create an annual budget calculation using excel assuming the following monthly expenditures:

- Rent ($800)

- Utilities ($150)

- Groceries ($400)

- Clothes ($100)

- Miscellaneous ($400)

- Before deciding which investment(s) into your long term goals you want to make, you need to think about paying back your student loan. Assuming you borrowed $20,000 in a federal student loan program at 4.7 % capitalized interest. Find the monthly minimum payment on the loan if the term is 20 years.

You may want to use this online calculator to compute the minimum payment: http://www.finaid.org/calculators/loanpayments.phtml (Note that you’ll have to leave a blank in the field “Minimum Payment”).

- With the money left you want to think about a smart investment. In what follows you will be presented with 4 scenarios. Complete calculations for each one of the investments, and decide which investment(s) would make most sense given your current financial situation. Justify your decision in one paragraph giving clear information about why the scenario(s) you chose to invest in are superior to those you decided not to invest in.

(Hint: It might make sense to invest in more than one of the scenarios.)

- You want to buy a car, as it would save you 2h of time compared to commuting by train to work each day. An installment plan offered by the car dealer comes with a 5% down payment, and after checking your credit your car dealer offers you a finance charge of 12%. How much will can you afford to pay each month for an installment plan of 6 years? How much would be the most expensive car you could afford?

- Assuming you want to make a small investment with the $5,000 your family gave you as a graduation present. You want to start a 2year CD to save up the amount needed for the down payment on your car purchase. Your bank offers you an interest rate that yields 1% interest compounded weekly. How much money will you have after 2 years?

- Would it make sense to invest the $5,000 into paying off a part of your student loan or to use the money toward the down payment of your car purchase? What would be the advantages in using the $5,000 toward either of these options? What would be the disadvantages? Support your answer with numerical evidence.

- Let’s say with the leftover income you decide you want to save toward a larger investment (such as the purchase of a house). Your bank offers you a savings investment plan (annuity) with 2.5% compounded annually. How much money would you be able to put toward the annuity per month? Use the following online annuity calculator to determine how much money you’d be able to save after a 10 year annuity: http://www.calculatorsoup.com/calculators/financial/future-value-annuity-calculator.php (Hint: Type 0% at the Growth Rate since this is not a growing annuity). How much interest did the annuity earn over the 10 years?

,

,