City Tech Quantitative Reasoning Program offers a review session for MAT 1190 students.

Date: Thur, May 19th

Time: 1pm-2pm

Room: N723

This workshop is first come first serve.

City Tech Quantitative Reasoning Program offers a review session for MAT 1190 students.

Date: Thur, May 19th

Time: 1pm-2pm

Room: N723

This workshop is first come first serve.

Title: “How to Lie with Statistics, Or: Why You Should Always Look Twice at Map“ (see the link below)

Speaker: Melanie Lorek (NYCCT – GC – NYCulture)

Abstract:

As always, pizza and refreshments will be served at 12:45pm and the presentation will start at 1pm. Feel free to stop by anytime and let interested students know about this event.

https://sites.google.com/site/mathclubcitytech/

Date: April 19 ,

,

Time: 1pm

Room: N718

This brief presentation will cover best practices for assessing academic programs. Participants will be exposed to broadly applicable strategies for conducting efficient and effective assessment. There will also be ample time to discuss assessment issues particular to City Tech.

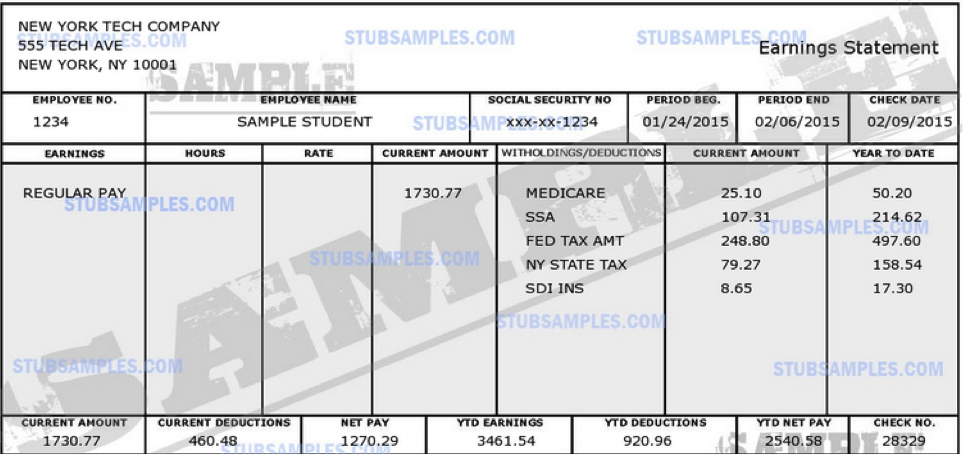

Click here to download the FinanceProject (PDF)

After graduating from NYCCT you landed a job earning 45k/ year. Congrats! Now it’s time to think about your long term life goals. Do you want to buy a car, a house, save for retirement, and attend grad school? Based on the information below and your bi-weekly income displayed in the pay stub below, compute the monthly costs for each scenario, and how long it would take to pay off each item. Remember that you’ll also have to pay off your student loan, and will need to cover your everyday living expenses.

This assignments consists of several steps:

You may want to use this online calculator to compute the minimum payment: http://www.finaid.org/calculators/loanpayments.phtml (Note that you’ll have to leave a blank in the field “Minimum Payment”).

(Hint: It might make sense to invest in more than one of the scenarios.)

Best Practices for Academic Assessment Dr. Marjorie Dorimé-Williams

Curriculum mapping by Dr. Marjorie Dorimé-Williams

The OpenLab is an open-source, digital platform designed to support teaching and learning at City Tech (New York City College of Technology), and to promote student and faculty engagement in the intellectual and social life of the college community.